Records show state office referred complaint to local government, which outsourced review to the agency’s own auditors and attorneys

LEXINGTON, Ky. — When a citizen filed a complaint with the Kentucky Auditor of Public Accounts alleging that the Lexington Convention and Visitors Bureau paid $284,000 in potentially unconstitutional bonuses using public tax revenue, the state’s top fiscal watchdog did not investigate.

Instead, records obtained through the Kentucky Open Records Act show, the auditor’s office passed the complaint to local government — which then let the tourism bureau’s own outside auditors and attorneys examine the allegations. Those hand-picked reviewers found no wrongdoing.

The arrangement raises questions about whether Auditor Allison Ball’s office fulfilled its oversight role and whether the review that ultimately took place was structured to reach a predetermined conclusion.

The complaint

Paul Oliva, a Lexington resident, submitted a tip to the auditor’s Digital Safe-House portal in April 2024 reporting that VisitLEX — the quasi-governmental agency that promotes tourism in Lexington using revenue from the city’s hotel tax — had distributed $284,745 in bonuses to staff in fiscal year 2024.

VisitLEX President Mary Quinn Ramer received the largest bonus at $56,507, bringing her total annual compensation to $339,043.

Oliva’s complaint alleged the bonuses violated Section 3 of the Kentucky Constitution, which prohibits public officers from receiving compensation beyond what is established for their services, and KRS 83A.070, which bars cities from paying bonuses or extra compensation to officers and employees unless specifically provided for by ordinance.

Oliva also flagged more than $427,000 in employee credit card charges at high-end restaurants and luxury hotels between July 2022 and March 2024, calling the spending a “gross waste and misuse of public funds.”

Passed along, not pursued

Rather than conduct its own examination, the auditor’s office sent a referral letter to Bruce Sahli, director of the Lexington-Fayette Urban County Government’s Office of Internal Audit, on Aug. 1, 2024.

The letter, signed by APA General Counsel Alexander Magera, stated that the allegations “do not reflect any findings or observations from any work performed by our office” and that the auditor took “no position on the validity of these claims.”

The referral asked LFUCG to investigate and report back.

But LFUCG’s own Department of Law immediately threw up an obstacle, opining that the Office of Internal Audit lacked legal authority to audit VisitLEX directly. Sahli described the situation in an email to the auditor’s office: “The LFUCG Department of Law opined that based upon the wording of the KRS that created VisitLEX, the LFUCG Office of Internal Audit does not have the authority to audit it.”

That legal opinion left the investigation in the hands of the entity being investigated.

VisitLEX investigates VisitLEX

With LFUCG unable to audit directly, the review was outsourced to VisitLEX’s own external auditors — the same accounting firm the bureau already employed. VisitLEX management met with the auditors and agreed to the scope and procedures.

The auditors themselves suggested that instead of conducting a full audit, they would perform a more limited set of Agreed-Upon Procedures, which test only specific assertions rather than providing a comprehensive opinion. Sahli agreed. VisitLEX, which by statute controlled the purse strings, also elected to have its auditing firm’s forensic services division handle the work, though Sahli noted he “did not consider this necessary.”

VisitLEX paid for the engagement. VisitLEX management helped define its scope. And at each stage, the parameters of the review were negotiated between LFUCG, VisitLEX, and VisitLEX’s auditors — with the state auditor’s office observing but not directing.

The legal opinion

In other words, the legal opinion at the center of the AUP report — the one that concluded VisitLEX was not subject to the bonus prohibition — was provided by a firm that VisitLEX was paying at least $60,000 a year to lobby on its behalf, using public tax dollars. Neither LFUCG nor the auditor’s office obtained an independent legal opinion or asked the Kentucky Attorney General to weigh in.

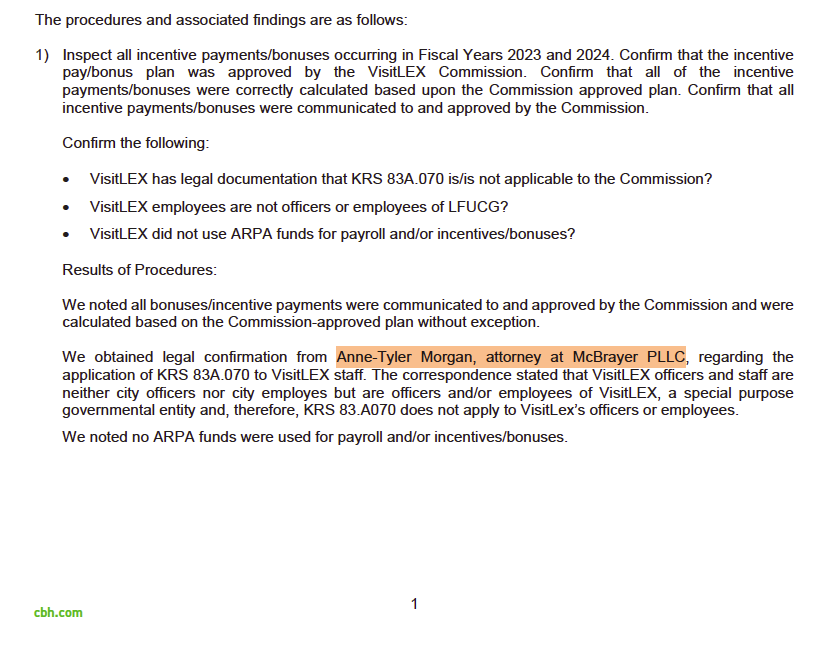

The most consequential finding in the resulting report, completed by accounting firm CBH on Feb. 25, 2025, concerned the constitutional question at the heart of Oliva’s complaint: whether the bonuses violated the law.

The auditors did not conduct an independent legal analysis. Instead, the report states: “We obtained legal confirmation from Anne-Tyler Morgan, attorney at McBrayer PLLC, regarding the application of KRS 83A.070 to VisitLEX staff.”

Morgan’s opinion concluded that VisitLEX officers and staff “are neither city officers nor city employees but are officers and/or employees of VisitLEX, a special purpose governmental entity and, therefore, KRS 83A.070 does not apply to VisitLex’s officers or employees.”

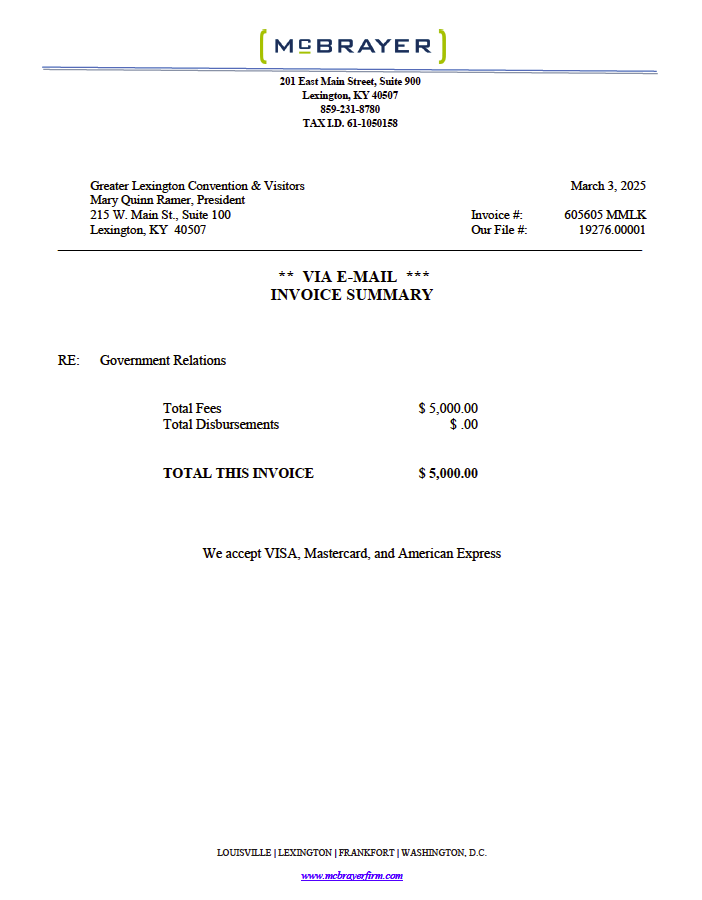

McBrayer PLLC is not simply VisitLEX’s outside counsel on this matter. Billing records obtained through a separate open records request show that the firm was simultaneously on a $5,000 monthly retainer with VisitLEX for “Government Relations” — lobbying work. An invoice dated March 3, 2025 — six days after the AUP report was finalized — billed VisitLEX for the March retainer, which was paid three days later on a VisitLEX credit card. Records show VisitLex paid 12 such monthly invoices in 2025.

In other words, the legal opinion at the center of the AUP report — the one that concluded VisitLEX was not subject to the bonus prohibition — was provided by a firm that VisitLEX was paying at least $60,000 a year to lobby on its behalf, using public tax dollars. Neither LFUCG nor the auditor’s office obtained an independent legal opinion or asked the Kentucky Attorney General to weigh in.

Questions about the legal argument

The McBrayer opinion raises significant questions.

VisitLEX is classified as a component unit of LFUCG in the city’s own financial reporting. It was created by city ordinance in 1974. Its nine commissioners are appointed by Lexington’s mayor. And it is funded entirely by the transient room tax — a public tax that LFUCG levies under KRS 91A.

The argument that VisitLEX employees are not city employees rests on its classification as a “special purpose governmental entity” under KRS Chapter 65A. But that chapter, enacted in 2013 to improve oversight and transparency of special districts, contains no provision exempting SPGEs from the constitutional prohibition on extra compensation. To the contrary, KRS 91A.360 requires tourist and convention commissions to comply with KRS 65A audit and governance requirements — suggesting the legislature intended more accountability for these entities, not less.

Moreover, Section 3 of the Kentucky Constitution is broader than KRS 83A.070. Even if VisitLEX employees are not technically “city employees” under the statute, the constitutional provision applies to public officers and those exercising public functions generally. VisitLEX staff manage and spend public tax revenue collected under state law for a purpose defined by state statute. Whether they hold the formal title of “city employee” may be irrelevant under the constitution.

The credit cards

On the $427,000 in credit card spending, the AUP review examined 134 of 3,032 transactions from fiscal years 2023 and 2024. Of those 134, the auditors found 9 that were submitted late — outside VisitLEX’s seven-day reimbursement window.

No other exceptions were noted. The report did not describe the nature of the expenses reviewed, identify spending at luxury hotels or high-end restaurants, or assess whether specific charges constituted a reasonable use of public funds.

The report itself states that it was “not engaged to, and did not, conduct an examination or review engagement, the objective of which would be the expression of an opinion or conclusion” on VisitLEX’s internal controls or legal compliance. It also acknowledged: “Had we performed additional procedures, other matters might have come to our attention that would have been reported to you.”

The auditor’s silence

Throughout the process, the state auditor’s office remained in contact with LFUCG. Jettie Sparks, an APA auditor, communicated with Sahli about sampling methodology and offered guidance on the AUP scope. The auditor’s office received the completed report.

But the office has taken no public action on the findings. It has not issued its own report. It has not challenged the McBrayer legal opinion. It has not referred the matter to the Attorney General for an independent legal determination.

When Oliva submitted an open records request in December 2025 seeking documents related to the auditor’s handling of his complaint, the office redacted all internal communications and withheld 32 emails entirely, claiming the matter remains “preliminary.” The auditor’s office maintained this position despite the fact that it referred the complaint to LFUCG 17 months earlier and the external review was completed 10 months before the records request.

A different standard

The auditor’s handling of the VisitLEX complaint stands in sharp contrast to how the office has treated similar conduct elsewhere.

In a separate examination of the City of Bedford, the auditor’s office found that cash payments of $75 to $150 labeled “bonus” or “Christmas bonus” violated Section 3 of the Kentucky Constitution. The auditor concluded that the payments — given to a small group of city employees with no authorizing ordinance — were precisely the kind of exclusive public emoluments the constitution prohibits. The office did not defer to the city’s judgment or accept a legal opinion from the city’s own attorneys. It applied the law and issued findings.

The auditor’s office also flagged a county attorney who awarded $134,500 in bonuses from restricted public revenues, including $126,500 to his own spouse, as likely unlawful under both constitutional and statutory limits.

In both cases, the auditor acted directly, conducted its own analysis, and published findings. The amounts involved were a fraction of the $284,745 VisitLEX distributed.

Yet when presented with a complaint involving bonuses nearly 2,000 times larger than Bedford’s Christmas checks, the auditor’s office referred the matter out, monitored from the sidelines as VisitLEX’s own professionals concluded the rules did not apply, and took no further action.

The auditor’s office has not explained why VisitLEX warranted a different approach.

The constitutional question, unanswered

The core legal issue — whether VisitLEX employees are subject to Section 3 of the Kentucky Constitution — remains unresolved. The only legal opinion on record is the one VisitLEX obtained from its own outside counsel. No court has ruled on the question. The Attorney General has not weighed in. And the state auditor, whose office has applied Section 3 against bonuses as small as $75 in other contexts, has declined to take a position.

Kentucky’s highest court held in Funk v. Milliken (1958) that public expenditures must be reasonable, for a public purpose, and not predominantly personal to the officer or employee. The auditor’s own reports have relied on this standard to strike down holiday bonuses, gifts, and similar payments across the state.

Whether that standard applies to a quasi-governmental agency that was created by city ordinance, is governed by mayoral appointees, is funded by a public tax, and is classified as a component unit of city government in LFUCG’s own financial statements is a question that, so far, no one with enforcement authority has been willing to answer.

The Auditor of Public Accounts did not respond to questions about the office’s handling of the complaint, including whether Auditor Ball had direct knowledge of the matter. VisitLEX and LFUCG have not publicly addressed the bonus allegations in the nearly two years since they were first reported.