In last week’s Meta, I discussed Lexington’s shaky financial situation. The City is facing unfunded pension obligations, heavy debt, and a potential $45M shortfall next year. We received over $100M in federal American Rescue Plan Act (ARPA) funds during the pandemic, but some say too much of those funds have been allocated to frivolous projects like new parks and trails. In fact, the ratio of our liabilities to liquid assets was enough for one think-tank to give Lexington a “D” in fiscal health.

Seemingly on cue, LFUCG-adjacent non-profit CivicLex released the following brief Monday in their weekly newsletter:

“At the Budget, Finance, and Economic Development Committee meeting, City Council will be hearing from Baird, a financial advisory firm that works with LFUCG. Representatives from Baird will present on the city’s bond rating as it relates to Lexington’s debt service. Baird’s report cites Lexington’s diverse economy and successful rebound from the pandemic as reasons for the City’s stable credit situation. You can view the full presentation here.“

Translation from government PR double speak:

“Due to the incoming $45M shortfall, the City is going to need to take on more bond debt this year to finance its operations. In order to soften the blow, the Gorton administration has hired consultants to prepare a report for Council that reports everything is just fine.“

The presentation will take place Tuesday, but since we have an advance copy of it, let’s take a sneak peak at what will be presented, versus what the actual numbers say.

Baird’s presentation begins by praising the management team for making some shrewd moves during the pandemic, which saved the city money by refinancing some old debt at lower interest rates:

By refinancing 3 bonds at lower interest rates, the city saved money during the pandemic.

By referencing a few pages later, we can see that these new bonds indeed had lower variable rates ranging from 0.35% to 1.68%.

Refinancing old bonds at historically low interest rates in 2020 was a shrewd move that saved the city money.

The provided data shows a rate for the Series 2013C bonds, which was 4.00% when originally issued. So far, so good.

The original 2013 bonds were financed at 4.00%

Historically favorable?

Did you notice the heading on that first slide? “Borrowing Rates Continue To Be Historically Favorable.” Let’s examine that claim.

Baird seems to focus on the moves the City made during the pandemic as a way of associating any future bonding with the fleeting opportunities the record-low interest rates of 2020 provided. But we can easily go to the next page and see that we’re no longer getting these artificially low rates: our two 2022 bond issues were financed at variable rates of 2.625% to 5.00%.

After interest rates rose, 2022 bonds were financed at rates as high as 5.00%

With this in mind, let’s examine Baird’s second slide, which provides an economic update and interest rate forecast:

Baird predicts that the SVB collapse will result in lower interest rates.

In this slide, Baird examines the economic climate following the Silicon Valley Bank collapse and predicts interest rates will increase by less than previously predicted, with the fed only slightly bumping rates at its coming meeting. Specifically, they predict a federal fund rate between 5.01% and 5.4% in Q3-Q4 of 2023, when any potential FY24 bonding would take place.

So… historically low, eh? Let’s see what the Federal Reserve thinks about that.

When Baird says “historically low” what they really mean is that interest rates haven’t been this high since 2007, but 30 years ago (you know, back in history) they tended to be much higher than they are now.

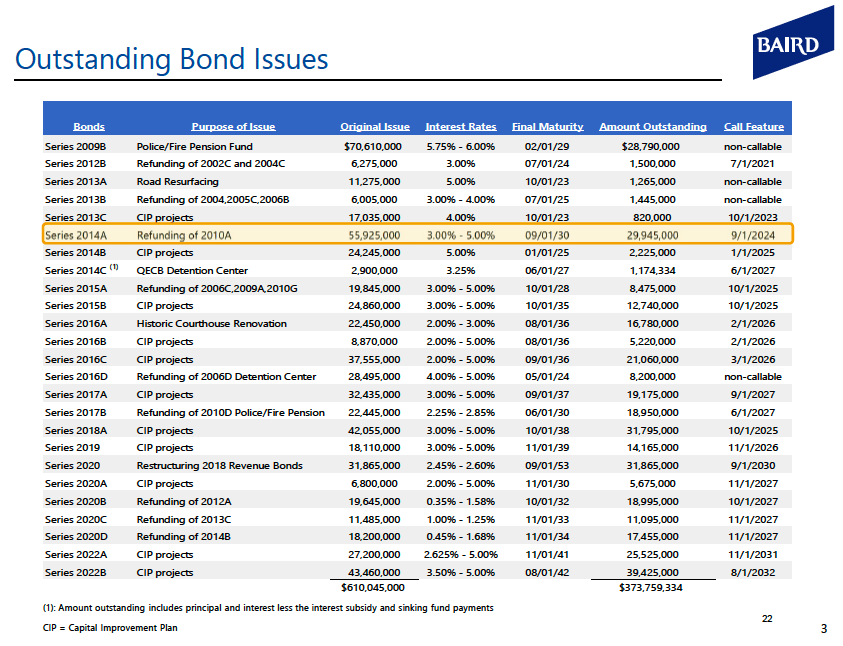

The presentation continues with a list of all LFUCG’s current bonds, which total $373.7M currently outstanding.

LFUCG outstanding bond issues

The next page is a (rather optimistic) breakdown of our future debt service that (almost laughably) assumes no future bonding whatsoever.

LFUCG future debt service, assuming no future bonding.

Big bonds coming

It should almost go without saying that this entire presentation is intended to make Lexington’s inevitable future debt more palatable to the Council and the average taxpayer. We’re looking at new bonds to cover general day-to-day operations, as well as our increasing unfunded Police & Fire Pension liabilities. Check out this slide from the Mayor’s budget retreat presentation:

The City projects a $45M budget shortfall in FY24

As the slide says, in FY24, the “level of bonded funds needs to be a serious conversation.” And for what it’s worth, it does appear possible that we could get through FY24 without taking on any new debt, as the city is reporting a $29M surplus for FY23 so far.

City FY23 budget shows a $29M surplus through Feb.

However, even though not taking on new debt could be an option this year, it remains to be seen if that’s the course the Mayor and Council will actually take. Additionally, the fact that the administration is having consultants give misleading presentations on the current “historically favorable” interest rates can be seen as an indicator that the Mayor will propose new bond issues in her coming proposed FY24 budget.

But even if we don’t bond this year, low unemployment in Lexington means revenue growth is likely to slow, and ARPA money will soon be drying up. Coupling these factors together, it appears more likely than not that we’ll need to bond in future years, even if we can avoid it this year.

Growing unfunded pension liabilities

Besides general government operations, another tricky area where bonding will likely soon be necessary is Police and Fire Pensions.

This isn’t a hard one, either: back on September 14, 2021, the Police and Fire Pension topped $1 billion market value for the first time ever. The city issue a victorious press release, spiked the football, and then proceeded to watch the fund sink to just under $850 million market value by July 2022, accruing even more unfunded pension liabilities the entire time. As of FY22, pension contributions covered only 46.27% of newly accrued liabilities, leaving us with a calculated $342M (and growing) in unfunded pension liabilities, as of July 1, 2022.

Given the current economic climate, I don’t feel overly optimistic that we’ll be able to trade our way out of this hole. While the current contributions are still considered “actuarially sound,” those calculations assume a steady return every year, a return that isn’t coming to fruition as we’d hoped. Eventually, the city will need to look at issuing bonds to cover these unfunded liabilities.

What to expect

Given the gaping $342M pension shortfall, along with growing operational deficits, we can likely expect the city to issue more new bond debt this year, and in the coming years. Eventually, though, probably around the time the Mayor leaves office in 2026, we’re going to hit a wall and face a hard choice: face deep cuts to city services, walk back our commitments to retired first responders, or raise taxes.

To whoever’s out there mulling a 2026 mayoral run: have fun with that.

This column has been updated to correct phrasing in the paragraph about projected interest rates.

Mon, March 20, 2023

Commentary, Featured, Lexington Meta, Local Government

Lexington Times Web Editor

In last week’s Meta, I discussed Lexington’s shaky financial situation. The City is facing unfunded pension obligations, heavy debt, and a potential $45M shortfall next year. We received over $100M in federal American Rescue Plan Act (ARPA) funds during the pandemic, but some say too much of those funds have been allocated to frivolous projects like new parks and trails. In fact, the ratio of our liabilities to liquid assets was enough for one think-tank to give Lexington a “D” in fiscal health.

Seemingly on cue, LFUCG-adjacent non-profit CivicLex released the following brief Monday in their weekly newsletter:

“At the Budget, Finance, and Economic Development Committee meeting, City Council will be hearing from Baird, a financial advisory firm that works with LFUCG. Representatives from Baird will present on the city’s bond rating as it relates to Lexington’s debt service. Baird’s report cites Lexington’s diverse economy and successful rebound from the pandemic as reasons for the City’s stable credit situation. You can view the full presentation here.“

Translation from government PR double speak:

“Due to the incoming $45M shortfall, the City is going to need to take on more bond debt this year to finance its operations. In order to soften the blow, the Gorton administration has hired consultants to prepare a report for Council that reports everything is just fine.“

The presentation will take place Tuesday, but since we have an advance copy of it, let’s take a sneak peak at what will be presented, versus what the actual numbers say.

Baird’s presentation begins by praising the management team for making some shrewd moves during the pandemic, which saved the city money by refinancing some old debt at lower interest rates:

By referencing a few pages later, we can see that these new bonds indeed had lower variable rates ranging from 0.35% to 1.68%.

The provided data shows a rate for the Series 2013C bonds, which was 4.00% when originally issued. So far, so good.

Historically favorable?

Did you notice the heading on that first slide? “Borrowing Rates Continue To Be Historically Favorable.” Let’s examine that claim.

Baird seems to focus on the moves the City made during the pandemic as a way of associating any future bonding with the fleeting opportunities the record-low interest rates of 2020 provided. But we can easily go to the next page and see that we’re no longer getting these artificially low rates: our two 2022 bond issues were financed at variable rates of 2.625% to 5.00%.

With this in mind, let’s examine Baird’s second slide, which provides an economic update and interest rate forecast:

In this slide, Baird examines the economic climate following the Silicon Valley Bank collapse and predicts interest rates will increase by less than previously predicted, with the fed only slightly bumping rates at its coming meeting. Specifically, they predict a federal fund rate between 5.01% and 5.4% in Q3-Q4 of 2023, when any potential FY24 bonding would take place.

So… historically low, eh? Let’s see what the Federal Reserve thinks about that.

When Baird says “historically low” what they really mean is that interest rates haven’t been this high since 2007, but 30 years ago (you know, back in history) they tended to be much higher than they are now.

The presentation continues with a list of all LFUCG’s current bonds, which total $373.7M currently outstanding.

The next page is a (rather optimistic) breakdown of our future debt service that (almost laughably) assumes no future bonding whatsoever.

Big bonds coming

It should almost go without saying that this entire presentation is intended to make Lexington’s inevitable future debt more palatable to the Council and the average taxpayer. We’re looking at new bonds to cover general day-to-day operations, as well as our increasing unfunded Police & Fire Pension liabilities. Check out this slide from the Mayor’s budget retreat presentation:

As the slide says, in FY24, the “level of bonded funds needs to be a serious conversation.” And for what it’s worth, it does appear possible that we could get through FY24 without taking on any new debt, as the city is reporting a $29M surplus for FY23 so far.

However, even though not taking on new debt could be an option this year, it remains to be seen if that’s the course the Mayor and Council will actually take. Additionally, the fact that the administration is having consultants give misleading presentations on the current “historically favorable” interest rates can be seen as an indicator that the Mayor will propose new bond issues in her coming proposed FY24 budget.

But even if we don’t bond this year, low unemployment in Lexington means revenue growth is likely to slow, and ARPA money will soon be drying up. Coupling these factors together, it appears more likely than not that we’ll need to bond in future years, even if we can avoid it this year.

Growing unfunded pension liabilities

Besides general government operations, another tricky area where bonding will likely soon be necessary is Police and Fire Pensions.

This isn’t a hard one, either: back on September 14, 2021, the Police and Fire Pension topped $1 billion market value for the first time ever. The city issue a victorious press release, spiked the football, and then proceeded to watch the fund sink to just under $850 million market value by July 2022, accruing even more unfunded pension liabilities the entire time. As of FY22, pension contributions covered only 46.27% of newly accrued liabilities, leaving us with a calculated $342M (and growing) in unfunded pension liabilities, as of July 1, 2022.

Source: https://www.lexingtonky.gov/sites/default/files/organization-page/2023-02/01.13.23%2007.01.2022%20Valuation%20Report%20%28FINAL-Exp%20Study%29.pdf

Given the current economic climate, I don’t feel overly optimistic that we’ll be able to trade our way out of this hole. While the current contributions are still considered “actuarially sound,” those calculations assume a steady return every year, a return that isn’t coming to fruition as we’d hoped. Eventually, the city will need to look at issuing bonds to cover these unfunded liabilities.

What to expect

Given the gaping $342M pension shortfall, along with growing operational deficits, we can likely expect the city to issue more new bond debt this year, and in the coming years. Eventually, though, probably around the time the Mayor leaves office in 2026, we’re going to hit a wall and face a hard choice: face deep cuts to city services, walk back our commitments to retired first responders, or raise taxes.

To whoever’s out there mulling a 2026 mayoral run: have fun with that.

This column has been updated to correct phrasing in the paragraph about projected interest rates.

Lexington Times Web Editor

Recommended Posts

No need to further victimize children through legislative ineptitude or gubernatorial stubbornness

Fri, July 26, 2024

Andy Beshear sees a path: running through J.D. Vance

Wed, July 24, 2024

Landowners, then and now

Mon, July 22, 2024