🌎 Resumen en español · traducción automática

Kentucky está reduciendo gradualmente su impuesto sobre la renta, bajando la tasa del 5 por ciento en 2022 al 3.5 por ciento a partir de enero de este año, pero una disposición legal de 2023 protege a los proyectos de financiamiento con incremento de impuestos aprobados antes de 2023 de sentir el impacto de estos recortes. La ley añadió un "modificador" que recalcula los ingresos de retención de impuestos sobre la renta como si la tasa nunca hubiera bajado del 5 por ciento, permitiendo que estos proyectos de desarrollo reciban subsidios completos a pesar de las reducciones fiscales generales del estado.

Traducción y resumen generados por IA a partir del artículo en inglés. Puede contener errores; consulte el texto original.

Kentucky is in the middle of a deliberate retreat from the income tax. A flat 5 percent rate held through 2022; lawmakers cut it to 4.5 percent for 2023, to 4 percent for 2024, and built a trigger mechanism meant to ratchet it toward zero. The rate has not fallen on a clean annual schedule — the triggers were missed for 2025, leaving the rate at 4 percent two years running, and missed again for 2027 by about $7.5 million — but it has fallen, to 3.5 percent effective this January. For most of what the income tax touches, a lower rate means less money collected. That is the point.

There is a category of state spending built to be immune. It sits in the documents the Department of Revenue produced for the Red Mile’s tax-increment-financing district — and it reaches far beyond the Red Mile.

How a TIF feels a rate cut — and how this one doesn’t

A tax-increment-financing district captures the growth in certain taxes generated inside its boundary and routes that increment back to the project instead of to the general fund. For most Kentucky TIFs, the largest single component is payroll withholding — the state income tax withheld from the paychecks of everyone working inside the footprint.

That creates an obvious mechanical consequence. When the state cuts its income-tax rate, less is withheld from those same paychecks, so the withholding increment — the subsidy — should shrink right alongside everyone’s tax bill. A project capturing 5-percent-rate withholding in 2022 should capture noticeably less at the 4 percent rate of 2024.

It doesn’t. A provision written into Kentucky law in 2023, and extended twice since, makes certain the cut never reaches the project.

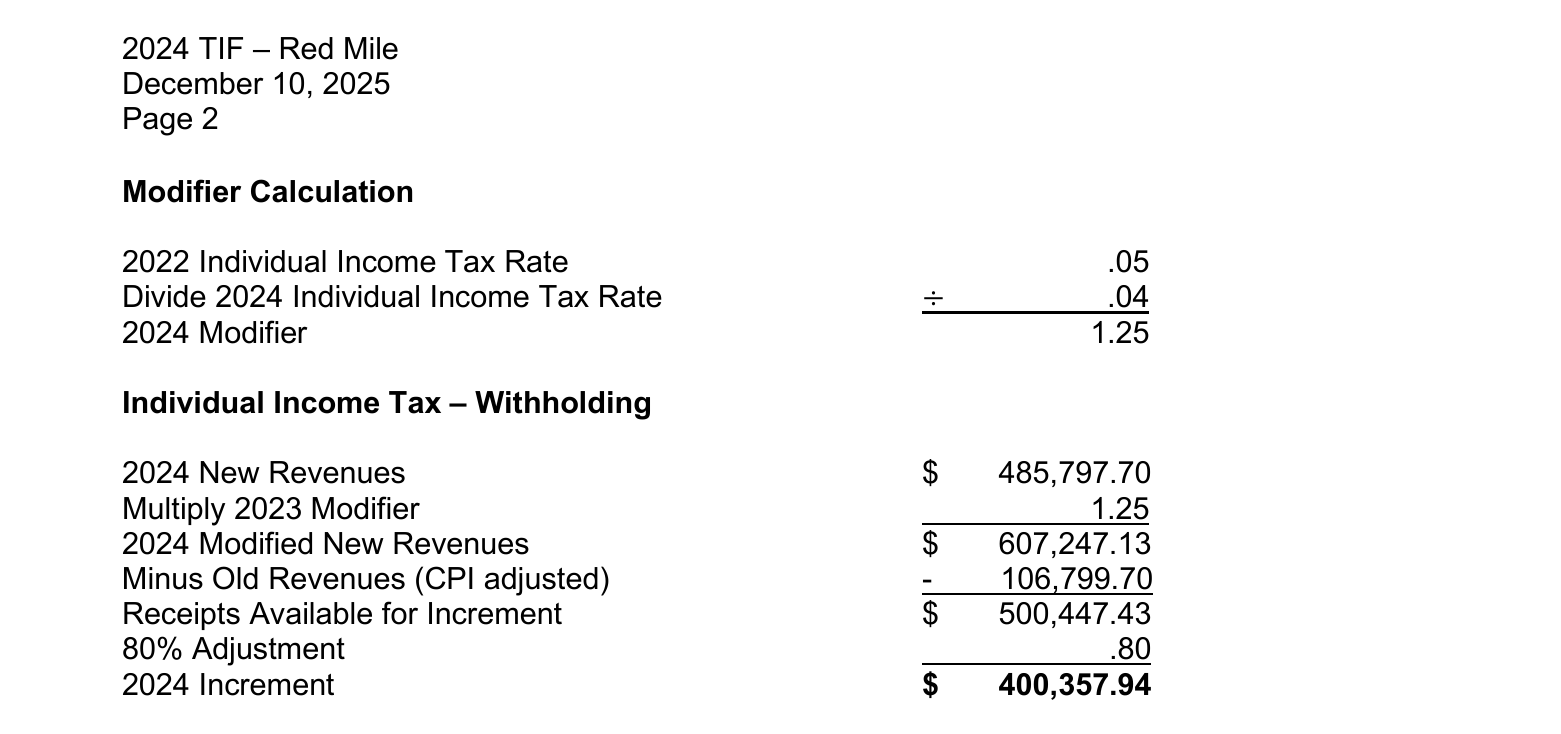

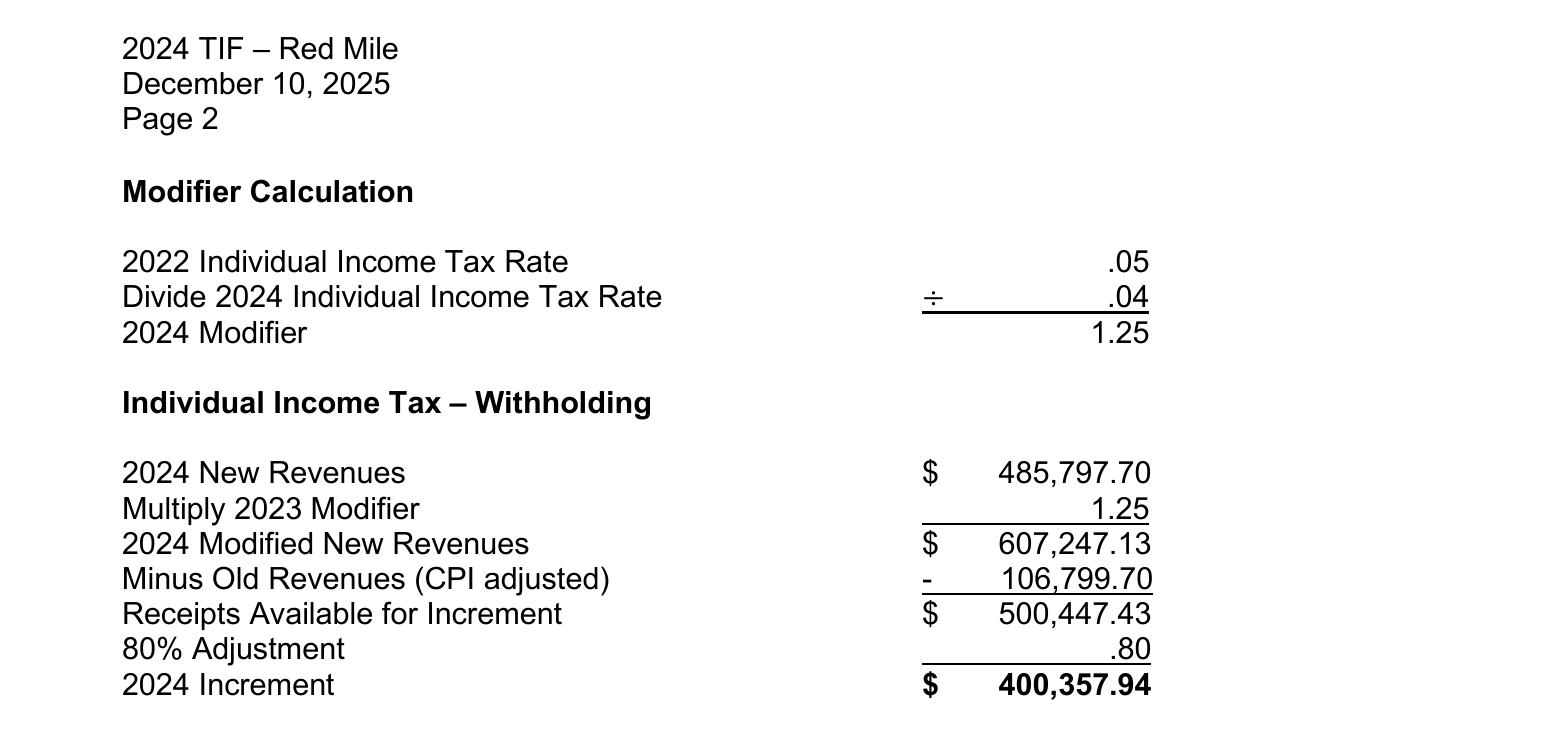

The “modifier”

The 2023 tax bill, House Bill 360, amended KRS 154.30-010, the statute defining how TIF increment is calculated, to add what the Revenue Department’s letters call a “modifier.” For any TIF project approved before January 1, 2023, the state takes the withholding actually generated inside the district and grosses it back up, as if the income-tax rate had never moved off 5 percent.

The formula is plain: the modifier is the 2022 rate of 5 percent divided by the rate in the year being calculated. As the denominator falls, the multiplier climbs:

- 2023 (4.5 percent): modifier 1.111

- 2024 (4 percent): modifier 1.25

- 2026 (3.5 percent): modifier 1.43

The Red Mile’s letters show the mechanism in operation. In 2023, the project’s actual payroll-withholding “new revenues” of $497,132 were grossed up to $552,369 before the increment was figured. In 2024, with the rate at 4 percent, $485,798 in actual withholding was inflated to $607,247 — a phantom $121,449 the paychecks never produced, added to the base the state then pays a share of.

That single adjustment is large enough to flip the arithmetic of the whole deal. In 2024 the Department of Revenue’s final increment of $623,434.93 came in roughly $82,000 above what Lexington had even requested — one of the only times in the record the state paid out more than the city asked for. The reason was the modifier: the state’s own formula valued the withholding at a rate Kentuckians no longer pay.

Who is held harmless, and at whose expense

Read sympathetically, the modifier has a logic. Developers structured these deals years ago on the expectation of a 5-percent-rate increment; a later, unrelated change in state tax policy would otherwise quietly rewrite the economics of agreements already signed. The modifier holds the bargain constant against a rule change the developer did not choose.

But the increment is not the developer’s money until the state diverts it. It is state revenue that would otherwise reach the general fund — schools, Medicaid, public safety, the things a 4 percent income tax still has to pay for. So the modifier draws a quiet line. When Kentucky cut the income tax, ordinary taxpayers got the smaller rate and the general fund absorbed the loss. But the subsidized projects were carved out and made whole: their share of the income tax is still calculated at 5 percent, and the gap is covered out of the same general fund now collecting less. The gross-up even holds in a year like 2025, when the trigger failed and lawmakers could not cut anyone’s rate — because it is keyed to the gap below 5 percent, not to any new cut.

And the design tilts one way: the further the rate falls, the larger the gross-up. It is 1.25 at a 4 percent rate and about 1.43 at the 3.5 percent rate now in effect — a withholding base inflated more than 40 percent above what the paychecks generate. The provision is not, on its face, open-ended: the statute runs the modified calculation only through calendar year 2026. But that ceiling has already been lifted twice. HB 360 wrote the gross-up for 2023 and 2024 alone; a 2024 act carried it forward, and a 2025 act extended it again to 2026. Each extension has tracked the income tax down. Whether it is renewed past 2026 — and how large the multiplier is allowed to grow as the rate keeps falling — is a live question for a future session, and one worth watching.

Not just the Red Mile

The Red Mile is simply the project whose letters are now public. By the statute’s own terms the modifier applies to every Kentucky TIF approved before January 1, 2023 that captures withholding. In Lexington alone that takes in Phoenix Park/CentrePointe, Coldstream Research Campus, the Lexington Center project and the Summit at Fritz Farm, with dozens more statewide. Kentucky has pledged up to $3.1 billion in future state taxes across two dozen such projects — and because the state publishes only each district’s ceiling, never its annual payout, the cumulative cost of grossing all of them back up to a retired tax rate is, like the payouts themselves, absent from any public ledger. The provision has drawn no public analysis since it was enacted; the Red Mile’s letters are the first place its arithmetic is visible. The Red Mile shows what one project’s slice looks like. The statewide total is, by law, nobody’s to see.

This article was reported and written by The Lexington Times (Paul Oliva) with AI assistance (Claude Opus 4.8) for research, fact-checking and drafting. The dollar figures and the modifier mechanics are taken directly from the Kentucky Department of Revenue’s Red Mile increment letters for 2023 and 2024 (open-records response O-26-52R). The legal framing is grounded in KRS 154.30-010 as enacted by HB 360 (2023) and extended by SB 129 (2024) and a 2025 act; the income-tax rate history in HB 8 (2022) and HB 1 (2025); and statewide TIF context from the Kentucky Center for Economic Policy. The image is an excerpt of the Department’s 2024 increment letter.

Republishing: This is original Lexington Times reporting, licensed under Creative Commons CC BY-ND 4.0. You may republish this article, in full and unaltered, for free — including commercially — with credit to The Lexington Times and a link to the original.